The Roth IRA isn’t usually associated with high earners. However, there is a way to provide the advantages of tax-free growth and tax-free withdrawals in retirement, even if you are over the income limits. An IRS loophole that allows for investment account conversions means that those who exceed the income limits for a Roth IRA can convert traditional IRA contributions into a Roth IRA. If you’ve contributed the maximum to tax-deferred accounts such as 401(k)s, additional savings that can grow tax-free may make sense, even if they don’t reduce your taxes in the year in which you contribute.

Using a backdoor Roth IRA strategy can be a powerful way to create additional retirement savings, but first, let’s understand what it looks like and when it makes sense to use it.

The Advantages of a Roth IRA

Since you pay taxes on the funds before they are contributed to the Roth IRA, no further taxes are due on withdrawal if you make qualified withdrawals. This means your money has the potential to grow tax-free.

Another advantage of investing in a Roth IRA is that it is not subject to required minimum distributions (RMDs). This allows for more control over the income stream in retirement, ensuring that income stays under the levels that would trigger taxes on Social Security benefits or the Medicare Part B surcharge.

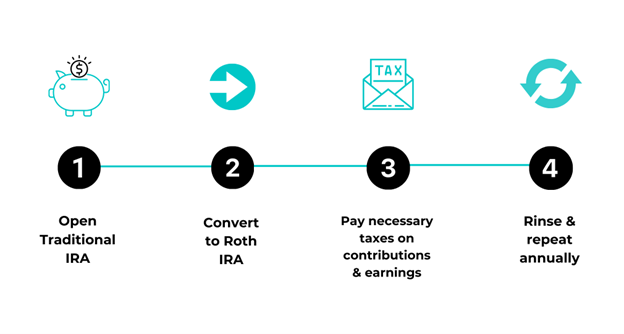

What is a Backdoor Roth IRA?

A Backdoor Roth IRA is a term applied to opening a traditional IRA account and immediately converting it to a Roth IRA. It gives high earners who typically wouldn’t fall under the income qualifications the ability to save additional, tax-free funds for retirement.

In 2022, the income limits to contribute to a Roth IRA are $144,000 for single filers or $214,000 for those who are married and file jointly. However, with a backdoor Roth IRA, you can convert a traditional IRA (which doesn’t have income limits) into a Roth IRA to receive the tax-free growth it provides.

How Does the Conversion Work?

The process is simple. You open a non-deductible, traditional IRA and contribute up to the maximum amount of $6,000 ($7,000 for age 50 and older), and then immediately convert to a Roth. In this scenario, the original amount is contributed to the IRA with after-tax dollars, and no further taxes are due. However, if it is allowed to sit in the traditional IRA account and it grows – taxes will need to be paid on the growth before it can be converted to a Roth IRA.

The Watch Out

If you have a traditional IRA funded for a few years, the investments have grown, or you’ve deducted contributions – or all the above – the rules around the taxation can be a little tricky. The IRS doesn’t allow an investor to single out non-deductible contributions within a traditional IRA when doing a Roth conversion.

The Drawbacks of Roth Conversions

There are a few things to consider before using the backdoor Roth IRA strategy.

First, you must have the Roth IRA established for five years after making the conversion before taking any withdrawals, or you’ll incur penalties, and you can’t withdraw earnings penalty-free with the full tax benefits until age 59 1/2.

Also, even though the Roth IRA can provide many benefits, if your tax bracket in retirement ends up being lower than it is right now, the conversion and tax-free aspect won’t be as impactful.

The Takeaway

Backdoor Roth IRAs are a powerful tool when used correctly and can provide tax advantages that other retirement accounts can’t. However, many different factors play a role in deciding whether to do a backdoor Roth IRA, so it’s recommended to talk with a CPA or financial advisor about your specific situation and run the numbers before committing to a conversion.